How to Screen Tenants with Bad Credit (Without Guessing)

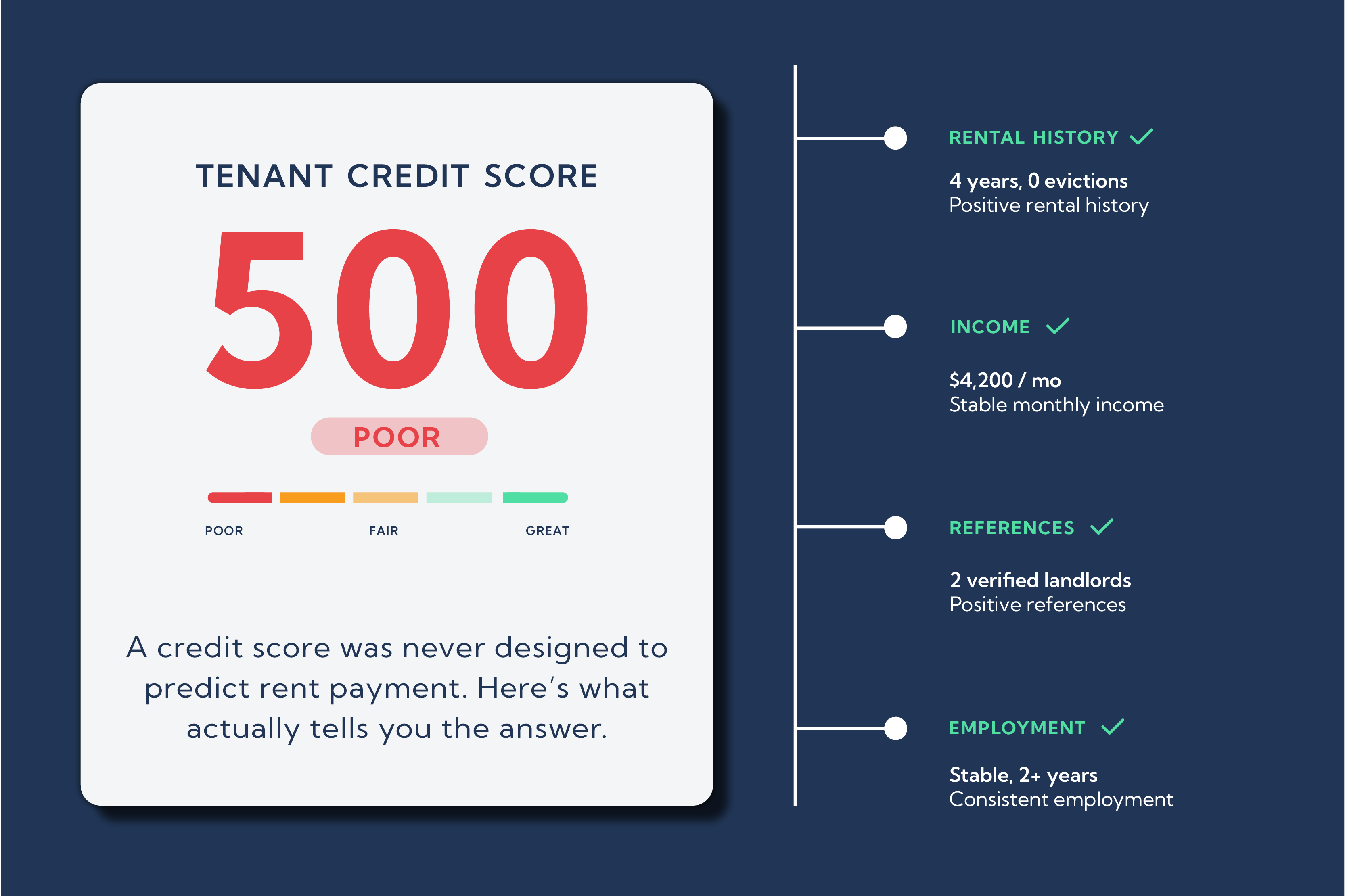

A qualified applicant walks in. Strong employment, two years at the same job, no evictions. But their credit score is 588.

Do you pass?

Most landlords are stuck using a blunt instrument - a three-digit number that was designed to predict credit card repayment, not whether someone will pay rent on time for 12 months. The result: good tenants get rejected, units stay vacant longer, and landlords wonder why their approval rates keep dropping.

Here's a better framework for screening tenants with low credit scores - one that looks at what actually predicts rental outcomes.

Why Credit Scores Are a Poor Proxy for Rental Risk

Credit scores were built by lenders to evaluate revolving debt behavior. Medical bills, student loans, a divorce - all of these can crater a score without saying anything about how reliably a person pays their rent every month.

The data backs this up. Applicants with scores below 650 who have consistent, on-time rent payment history default at rates comparable to applicants with scores in the 700s. The score alone misses the signal that matters most.

This is why so many operators are moving toward alternative data to evaluate applicants - not to lower standards, but to get a more accurate picture of rental risk.

What to Look at Instead (or In Addition To) a Credit Score

When you're screening an applicant with a low credit score, you're really asking one question: Can this person reliably pay rent? Here's how to actually answer it.

1. Bank transaction history

This is the most underused signal in tenant screening. A direct connection to an applicant's bank account - with their permission - shows you 12 months of actual behavior: whether they pay recurring bills on time, whether their income is stable, and whether their spending patterns are consistent with their stated rent budget.

No paystub can tell you what bank data can. A person can hand you a doctored paystub. They cannot fabricate 12 months of timestamped transactions.

2. Verified income and employment

Require income verification, not just documentation. There's a difference between someone showing you a pay stub and a platform confirming active employment and income directly from the payroll source. Look for applicants earning at least 2.5–3x the monthly rent in verifiable income. If an applicant with a 580 credit score earns $6,000/month and their rent is $1,800, the math works - and the credit score may reflect old medical debt or a thin file, not a pattern of financial unreliability.

Rent Butter's income and employment verification tools connect directly to payroll systems so operators can see verified income without waiting on paperwork.

3. Rent payment history

Eviction records are a lagging indicator - by the time an eviction is filed, a situation has already gone badly wrong. What you really want to know is whether this person has a pattern of paying rent on time. Ask for landlord references and cross-check against any rental history data available in the screening report.

4. Context behind the score

A 610 credit score from a 24-year-old with two years of employment history and a thin file reads differently than a 610 from someone with three active collections accounts from the past six months. The number is the same. The risk is not.

Look at the breakdown of what's pulling the score down. Medical debt, student loans, and a single missed payment from years ago are very different from maxed-out credit cards and recent delinquencies on multiple accounts.

The Right Decision Framework

Here's a practical approach for evaluating low-credit applicants without guessing:

- Set a minimum income threshold, not just a minimum credit score. An income-to-rent ratio of 2.5–3x is a stronger predictor of payment reliability than a FICO cutoff.

- Require bank-verified income rather than paystubs alone. This removes fraud risk and gives you a real view of spending behavior.

- Check rental history and contact previous landlords. A clean rental history with one prior landlord reference is worth more than a credit score bump.

- Understand what's in the credit report. If the derogatory marks are medical, student, or old - and rent-related accounts are clean - that applicant often performs well.

- Use a standardized process for every applicant. This is a fair housing requirement as much as it's a business practice. Applying different criteria to different applicants creates legal exposure. Our free tenant screening checklist gives you a consistent framework you can apply across your portfolio.

What This Looks Like in Practice

Consider two applicants with the same 601 credit score.

Applicant A: The score is driven by $14,000 in medical collections from a 2021 hospitalization. They've had the same job for four years. Their bank statements show rent paid on the first of every month for the past three years, no overdrafts, and a monthly surplus after expenses. Income is 3.2x the rent amount.

Applicant B: The 601 reflects two recently opened credit cards at 90% utilization, a late car payment from last month, and a missed utilities bill. Income is 2.1x rent, and they've moved three times in 18 months.

The credit score is identical. The risk is not. A screening process that treats both applicants the same is working with incomplete information.

This is exactly the kind of nuance that Rent Butter's screening platform is built to surface - giving operators a clear picture of financial behavior, not just a number, so they can approve more qualified residents and reduce bad debt at the same time.

The Bottom Line

A low credit score is a reason to look harder, not a reason to walk away. The landlords who are consistently filling units with reliable tenants aren't lowering their standards - they're looking at better data.

Bank transaction behavior, verified employment, and clean rental history are stronger predictors of on-time rent payment than a credit score built for a different purpose. Use them.

If you want to see how Rent Butter approaches screening for applicants across the credit spectrum, learn more about how our platform works.