The Landlord's Guide to Tenant Income Verification in the Age of AI Fraud

A property manager receives an application that looks solid. The pay stubs show steady income. The gross-to-net math checks out. The employer name and address are real. She runs the documents through her fraud detection tool. Clean. She approves the lease.

Sixty days later, the tenant stops paying. A call to the employer reveals they've never heard of the applicant.

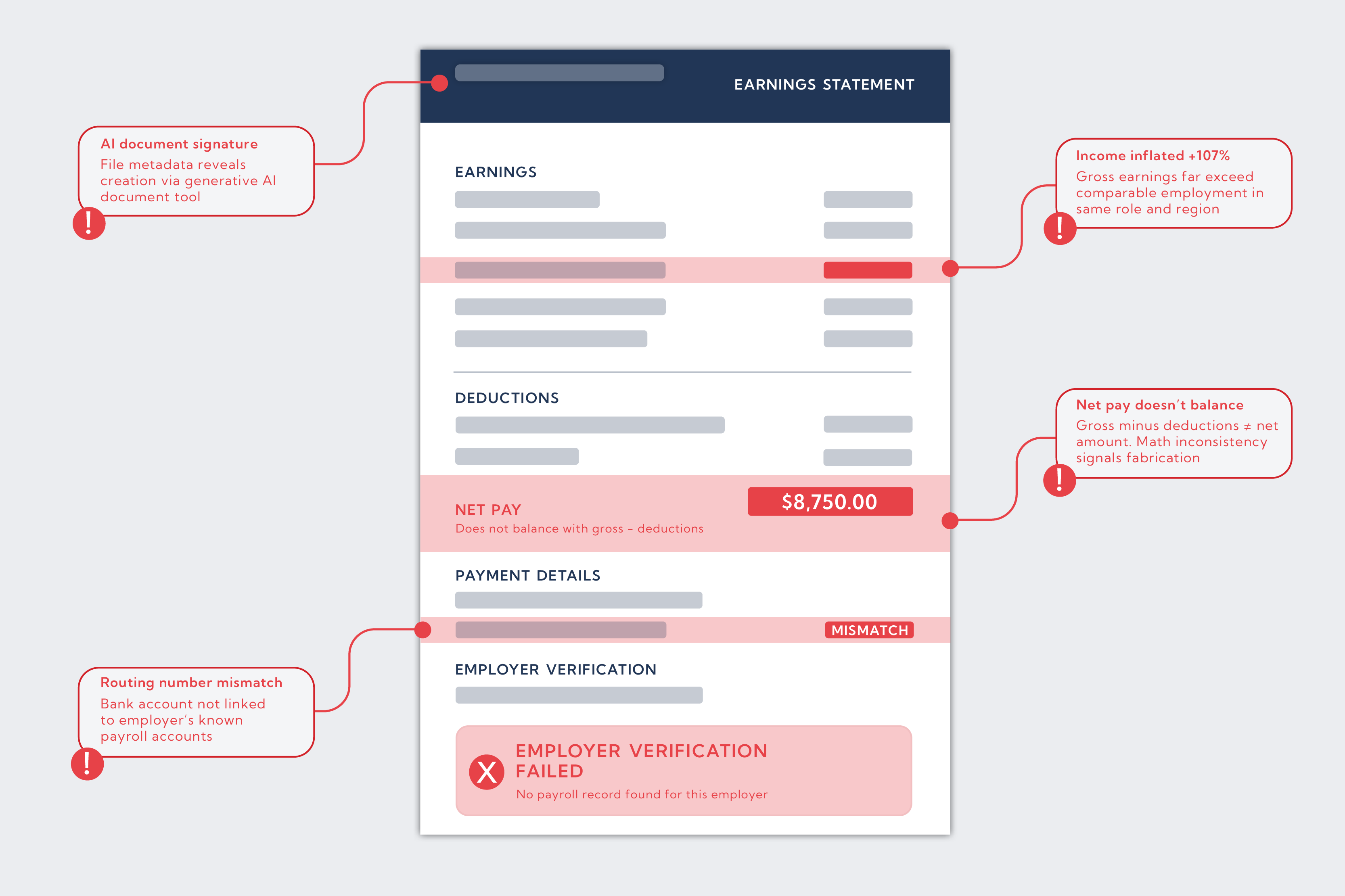

This isn't a story about carelessness. It's a story about a verification method that no longer works. AI-generated income documents increased 500% between April and December 2025, according to Snappt's fraud research. Today's fake pay stubs aren't the blurry Photoshop jobs of five years ago — they're built from scratch with correct math, real employer formatting, and plausible year-to-date figures. In a 2025 NMHC survey, 93% of property management respondents reported experiencing document-based fraud in the prior year.

If your income verification process relies on reviewing what applicants hand you, it's time to rethink it.

Why Document Review Has a Fundamental Flaw

For decades, the standard approach has been to collect pay stubs, W-2s, bank statements, and employer letters, then check them for red flags — rounded numbers, math errors, suspicious fonts. The advice hasn't changed much because, for a long time, it worked.

That advice assumes documents are the verification. They're not. A document tells you what someone claims about their income. A payroll system or bank account tells you what their income actually is.

The shift happened fast. Free AI tools can now generate convincing pay stubs in seconds. Metadata can be scrubbed. Fonts can be matched. The only way to catch these fakes is with AI detection tools — and even those are losing the arms race. As one fraud research firm put it bluntly: AI-generated pay stubs are now undetectable by most document review systems. The solution isn't better detection. It's eliminating the document from the process.

Direct-Source Verification: How It Works

Direct-source income verification bypasses the document entirely. Instead of reviewing submitted files, the screening platform connects directly to the applicant's payroll provider or bank account — with the applicant's consent — and pulls the data from the original source.

Payroll API connections work by authenticating into the employer's payroll system (through integrations with providers like ADP, Workday, Gusto, and hundreds of others) and returning verified income, employment status, and pay frequency directly. The data is live. It cannot be manually altered before it reaches you.

Bank transaction analysis goes further. Rather than just confirming a paycheck amount, it examines the actual deposit pattern over three to six months: How consistent are the deposits? Are the amounts stable? Are there recurring outflows that suggest debt obligations not disclosed on the application?

This is the approach Rent Butter uses — analyzing real bank transaction data to assess whether a tenant's actual financial behavior matches their stated income. It's particularly useful for screening applicants with non-traditional income: gig workers, self-employed tenants, freelancers. For these applicants, a single pay stub is nearly meaningless anyway. Two years of consistent bank deposits is not. See why alternative data beats credit scores for a deeper look at what direct financial data reveals that documents can't.

What to Actually Evaluate When You Have Real Data

Getting connected to a payroll or bank feed is only half the job. Here's how to read what you're looking at:

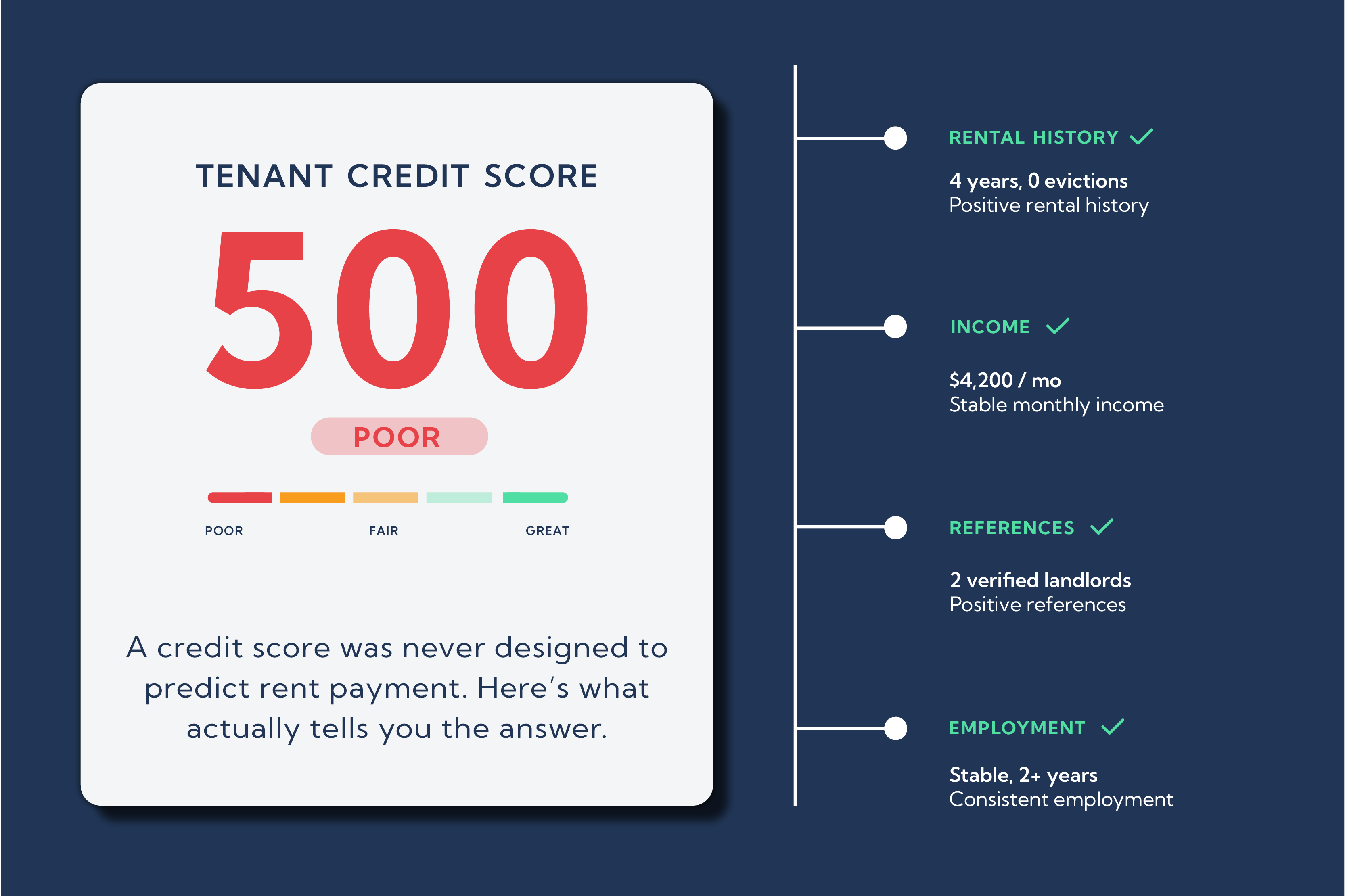

Consistency over magnitude. A tenant earning $4,200/month who has deposited between $4,050 and $4,350 for eight consecutive months is a fundamentally different risk profile than one who shows $7,000 in one month and $2,100 the next. Income volatility isn't automatically disqualifying, but unexplained swings deserve a closer look.

Deposit timing relative to rent due. If rent is due on the first, does income arrive before then? A misaligned pay schedule creates structural payment risk even when income is technically sufficient. A biweekly paycheck that consistently lands on the 5th and 20th is worth noting if your lease is due on the 1st.

Competing obligations. Bank transaction analysis can surface recurring payments that don't appear on a credit report — regular large transfers, recurring cash-out patterns, or consistent payments to multiple creditors. These tell you whether the income that looks adequate on paper is already committed elsewhere before rent is even factored in.

Net income, not gross. The 3x rent multiplier should be applied to verified net income — what actually lands in the account after taxes and deductions — not gross figures claimed on a document. A tenant showing $90,000/year in gross income may take home $5,200/month after taxes and benefits. If rent is $2,100, you're looking at a 2.5x ratio, not 3x. That distinction matters.

The Thin-File Problem

Standard income verification methods break down when applicants have limited credit histories — recent immigrants, young renters, or people rebuilding after financial hardship. These applicants often have stable, genuine income that simply doesn't show up through conventional screening.

A 26-year-old with $52,000 in W-2 income and no credit history looks riskier under standard models than they actually are. Real bank transaction data tells a different story: eight months of consistent direct deposits, no overdrafts, regular small transfers to savings. That's a reliable tenant — and a competitive opportunity for landlords willing to look past the credit score.

Rent Butter's screening solutions are built specifically around this gap — using alternative financial data to surface the payment behavior that credit models can't see. For operators looking to increase occupancy without increasing risk, expanding who you can confidently approve is a direct competitive advantage in any rental market.

Building Consistency Into Your Process

Properties that get hurt by income fraud most often are those making verification decisions inconsistently — thorough reviews for some applicants, lighter checks for others. Fraud exploits gaps.

A standardized screening process applies the same income verification method to every applicant. It removes subjectivity, creates a defensible paper trail, and makes it significantly harder for bad actors to game the system by submitting more polished fakes. It also helps with fair housing compliance — documenting that the same standard was applied uniformly across all applicants.

If your current workflow still relies primarily on reviewing submitted documents, a direct-source verification layer is worth evaluating. The math is simple: one fraudulent placement costs $7,000–$15,000 after eviction, lost rent, and unit turnover. Prevention is cheaper by every measure.

For landlords and property managers looking to build a screening process that doesn't depend on trusting what applicants hand you, Rent Butter's approach to screening — built around real financial data rather than documents — is worth a close look.