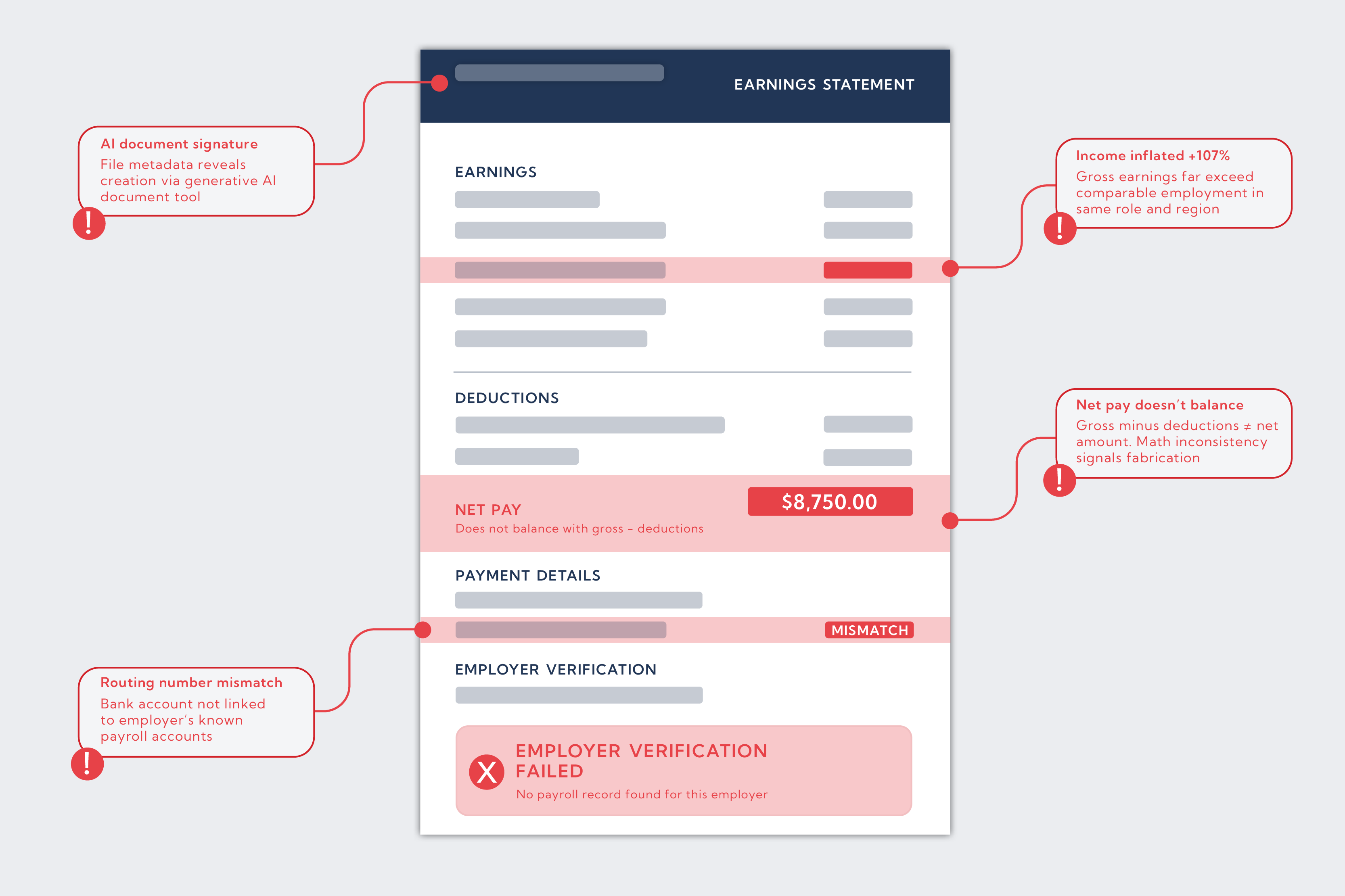

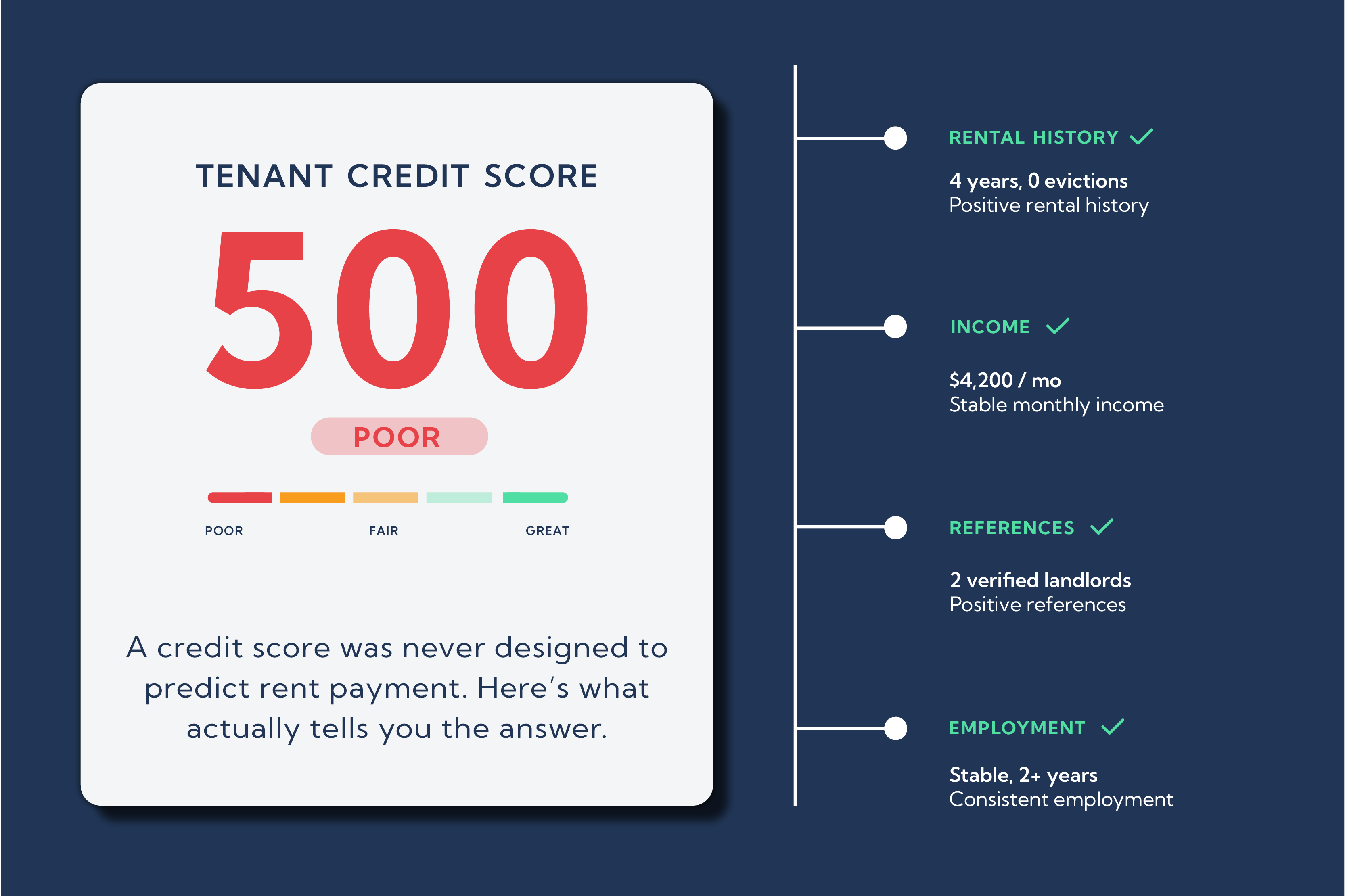

Credit Scores Aren't Everything

Every leasing team has met the “almost perfect” applicant — steady income, positive references, great demeanor - but a credit score that doesn’t meet policy. Rejecting that applicant feels safe, but it often means turning away a reliable resident.

Traditional credit data misses context. It tracks credit card debt and loan repayment, not whether someone pays rent on time. In today’s economy of freelancers and contractors, a thin credit file is common - and not a red flag.

The Rise of Behavior-Based Screening

Rent Butter looks beyond a single score to understand real financial behavior. By connecting securely to verified bank accounts and income streams, we measure:

- Consistent rent and bill payments

- Stable cash flow and savings habits

- Employment and deposit regularity

This data creates a clear picture of affordability and reliability that a credit bureau can’t.

Fairness and Speed Can Coexist

Automation turns what used to be manual back-and-forth into a one-day decision. Applicants verify their income digitally, and property managers receive an instant risk score based on actual cash flow rather than legacy credit.

That means fewer good renters lost to bureaucracy — and fewer vacant days on your ledger.

Compliance Built In

Every approval and adverse decision is tracked for FCRA and Fair Housing compliance. By standardizing criteria and using verifiable data, you can expand your applicant pool without adding risk.

Outcome: Better Approvals, Better Communities

Property managers who adopt alternative data report higher conversion rates and lower default rates. When approval is based on facts instead of assumptions, everyone wins — including your bottom line.